Volume 1, Columns

SL economy in doldrums amidst political chaos

April 19, 2018

While the Sri Lankan economy is on a downward path, the coalition government is struggling for its survival, and the economy is not on its radar.

The political front is in chaos. Conflicts within and among the ruling political parties have escalated since the local government elections held early this year. The government managed to win the no-confidence motion against Prime Minister Ranil Wickremesinghe but not without much effort. Some Ministers have resigned from their portfolios over the no-faith motion.

Meanwhile, the President has prorogued Parliament with effect from April 12, 2018. Amidst political turmoil, the country is further engulfed by the debt crisis with the US dollar 2.5 billion international sovereign bond offering by the Central Bank made just before the New Year festival. The new US dollar 1.25 billion five-year and US dollar 1.25 billion 10-year bonds were issued on April 11, 2018, and successful offers were received the same day. The Central Bank proudly claims that this represents the largest offshore bond offering ever by Sri Lanka and is a strong reflection of the international investor community’s continued support for Sri Lanka through the years.

However, it should be noted that it is not an easy task to pay back these massive foreign loans over the next 5 to 10 years, given the country’s extremely weak external finance situation and fiscal vulnerabilities. The government has not been successful in implementing any economic policy strategy or structural reform during its tenure. There is hardly any time left for the government to launch any long-term economic programme, as the Presidential and Parliamentary elections are due from next year onwards. The political turmoil has severe economic repercussions. It has created uncertainties in the market adversely affecting domestic, private and foreign investments.

[caption id="attachment_919" align="alignleft" width="5184"] Unemployment is highest amongst the youth and the educated.[/caption]

Political interests take precedence over economic compulsions

In Sri Lanka, little attention is paid to economic realities in the midst of the continuing political turmoil. As a result, the country has failed to reap the benefits of economic liberalisation over the last four decades, while many neighboring countries are forging ahead with faster economic growth though they launched economic liberalization much later. The bitter truth is that there are no short cuts to economic growth or development. It is only through the hard way that we can achieve it. The longer we postpone taking corrective steps the longer we have to wait for economic progress. The political economy has considerable bearing on socioeconomic development, as it is the political authority that ultimately determines development policies. These policies are not always optimal, and very often, politicians take the decisions at discretion for their own political survival, with a short-term focus ignoring long-term economic repercussions.

To satisfy voters in a bid to retain power, politicians have a tendency to offer various welfare benefits to households at every election, such as handouts, cash transfers and food subsidies and to also create jobs in the public sector. Such populist policy preferences invariably lead to an increase in government expenditure, budget deficit, public debt, the money supply, inflation and balance of payments deficits. The outcomes are the high cost of living, food shortages, subsidy cuts and various other hardships. Although the masses, particularly the poor, are said to be the beneficiaries of populist policies, they are the most adversely affected group due to the second-round effects of such policies. The much-needed structural reforms relating to foreign trade, foreign investment, state-owned enterprises and fiscal consolidation have been neglected over the decades. The results have been catastrophic. Economic growth never picked up to ease the problems of unemployment, poverty and income inequality. Also, the economy has been subject to severe instability due to budget and balance of payment deficits.

Mismanaging the economy

The current government has failed to adopt necessary economic policy strategies and structural reforms to address the above-mentioned growth setback and macroeconomic instability. The PM has presented several economic policy statements to Parliament from time to time, but to no avail. They contained some optimistic economic targets without any action plans. Most of the proposals mentioned in those statements were not implemented. They are also at variance with the proposals, contained in the consecutive budget speeches. Similar weaknesses could be found in the policy document titled, ‘Vision-2025: A Country Enriched’, launched by the government in August last year. The launching event seemed to have been designed to attract the youth with choreographic acts in an ultra-modern stage setting. Several youth who appeared on the stage, along with the President and the Prime Minister, posed some questions to the two leaders. The V2025 booklet, consisting of around 50 pages, had a long wish list to be fulfilled during the next 8 years. Surprisingly, it does not elaborate on the specific policy strategies to be implemented to achieve the envisaged objectives. It also does not contain any statistical tables or charts which would have been useful to substantiate the facts behind the Vision. The document looked more like a hurriedly-prepared election manifesto than a coherent policy document addressing the structural weaknesses in the economy. It contains a long list of “We will …” statements. This implicitly indicates that the political authorities are yet to introduce the much-needed policies. The Vision 2025 document states, “Over the next three years, within the 2025 Vision, we will implement a comprehensive economic strategy to address constraints to growth. We will aim to raise per capita income to USD 5,000 per year, create one million jobs, increase FDI to USD 5 billion per year and double exports to USD 20 billion per year. These intermediate targets lay the foundation for our Vision 2025: Sri Lanka to become an upper-middle income country.”

[caption id="attachment_920" align="alignleft" width="2500"]

Unemployment is highest amongst the youth and the educated.[/caption]

Political interests take precedence over economic compulsions

In Sri Lanka, little attention is paid to economic realities in the midst of the continuing political turmoil. As a result, the country has failed to reap the benefits of economic liberalisation over the last four decades, while many neighboring countries are forging ahead with faster economic growth though they launched economic liberalization much later. The bitter truth is that there are no short cuts to economic growth or development. It is only through the hard way that we can achieve it. The longer we postpone taking corrective steps the longer we have to wait for economic progress. The political economy has considerable bearing on socioeconomic development, as it is the political authority that ultimately determines development policies. These policies are not always optimal, and very often, politicians take the decisions at discretion for their own political survival, with a short-term focus ignoring long-term economic repercussions.

To satisfy voters in a bid to retain power, politicians have a tendency to offer various welfare benefits to households at every election, such as handouts, cash transfers and food subsidies and to also create jobs in the public sector. Such populist policy preferences invariably lead to an increase in government expenditure, budget deficit, public debt, the money supply, inflation and balance of payments deficits. The outcomes are the high cost of living, food shortages, subsidy cuts and various other hardships. Although the masses, particularly the poor, are said to be the beneficiaries of populist policies, they are the most adversely affected group due to the second-round effects of such policies. The much-needed structural reforms relating to foreign trade, foreign investment, state-owned enterprises and fiscal consolidation have been neglected over the decades. The results have been catastrophic. Economic growth never picked up to ease the problems of unemployment, poverty and income inequality. Also, the economy has been subject to severe instability due to budget and balance of payment deficits.

Mismanaging the economy

The current government has failed to adopt necessary economic policy strategies and structural reforms to address the above-mentioned growth setback and macroeconomic instability. The PM has presented several economic policy statements to Parliament from time to time, but to no avail. They contained some optimistic economic targets without any action plans. Most of the proposals mentioned in those statements were not implemented. They are also at variance with the proposals, contained in the consecutive budget speeches. Similar weaknesses could be found in the policy document titled, ‘Vision-2025: A Country Enriched’, launched by the government in August last year. The launching event seemed to have been designed to attract the youth with choreographic acts in an ultra-modern stage setting. Several youth who appeared on the stage, along with the President and the Prime Minister, posed some questions to the two leaders. The V2025 booklet, consisting of around 50 pages, had a long wish list to be fulfilled during the next 8 years. Surprisingly, it does not elaborate on the specific policy strategies to be implemented to achieve the envisaged objectives. It also does not contain any statistical tables or charts which would have been useful to substantiate the facts behind the Vision. The document looked more like a hurriedly-prepared election manifesto than a coherent policy document addressing the structural weaknesses in the economy. It contains a long list of “We will …” statements. This implicitly indicates that the political authorities are yet to introduce the much-needed policies. The Vision 2025 document states, “Over the next three years, within the 2025 Vision, we will implement a comprehensive economic strategy to address constraints to growth. We will aim to raise per capita income to USD 5,000 per year, create one million jobs, increase FDI to USD 5 billion per year and double exports to USD 20 billion per year. These intermediate targets lay the foundation for our Vision 2025: Sri Lanka to become an upper-middle income country.”

[caption id="attachment_920" align="alignleft" width="2500"] The newly put together National Economic Council, appointed and Chaired by President Sirisena will supersede the Cabinet Committee on Economic Management, chaired by Prime Minister Wickremesinghe.[/caption]

These are unattainable optimistic targets, as has been argued previously in my newspaper articles. However, the fate of this Vision document is unknown today. The outcome of the high-profile Sri Lanka Economic Forum held in Colombo in January 2016, too, is not evident. Several presentations were made at the Forum by some prominent experts from Harvard. As I reiterated in my newspaper columns, those presentations were mere reproductions of the age-old textbook stuff relating to export-constrained economic growth, low government revenue, structural transformation, urbanization and economic growth. However, all those grand events seem to have been forgotten by the policymakers now. Such foreign experts hardly offered any policy options to help overcome the economic problems facing a developing country like Sri Lanka. The ill-advised policies based on such deliberations are bound to have disastrous spill-over effects in the future for which no one would be held accountable, and the ordinary citizens will have to pay the price. This is the tragedy of the voiceless common people.

Recently, President Sirisena appointed a new National Economic Council (NEC) under his chairmanship to take key decisions on all the economic and development projects of the government.

The NEC is said to supersede the Cabinet Committee on Economic Management (CCEM), which is chaired by PM Wickremesinghe. It is not yet clear how these parallel bodies would demarcate their functions and duties. All these point to market uncertainties deterring the country’s potential to ease the hardships faced by the ordinary people, as discussed below.

Socioeconomic problems aggravating

Poverty, income disparities and unemployment are some of the burning socioeconomic problems, faced by the ordinary people in recent decades. The headcount poverty index declined from a peak level of 28.8 percent in 1995/96 to 4.1 percent 2016, according to the Department of Census and Statistics. These poverty indicators are based on the conventional poverty line which is measured only in terms of household expenditure, and therefore, do not capture the dimensions of overall quality of life, noted earlier.

The newly put together National Economic Council, appointed and Chaired by President Sirisena will supersede the Cabinet Committee on Economic Management, chaired by Prime Minister Wickremesinghe.[/caption]

These are unattainable optimistic targets, as has been argued previously in my newspaper articles. However, the fate of this Vision document is unknown today. The outcome of the high-profile Sri Lanka Economic Forum held in Colombo in January 2016, too, is not evident. Several presentations were made at the Forum by some prominent experts from Harvard. As I reiterated in my newspaper columns, those presentations were mere reproductions of the age-old textbook stuff relating to export-constrained economic growth, low government revenue, structural transformation, urbanization and economic growth. However, all those grand events seem to have been forgotten by the policymakers now. Such foreign experts hardly offered any policy options to help overcome the economic problems facing a developing country like Sri Lanka. The ill-advised policies based on such deliberations are bound to have disastrous spill-over effects in the future for which no one would be held accountable, and the ordinary citizens will have to pay the price. This is the tragedy of the voiceless common people.

Recently, President Sirisena appointed a new National Economic Council (NEC) under his chairmanship to take key decisions on all the economic and development projects of the government.

The NEC is said to supersede the Cabinet Committee on Economic Management (CCEM), which is chaired by PM Wickremesinghe. It is not yet clear how these parallel bodies would demarcate their functions and duties. All these point to market uncertainties deterring the country’s potential to ease the hardships faced by the ordinary people, as discussed below.

Socioeconomic problems aggravating

Poverty, income disparities and unemployment are some of the burning socioeconomic problems, faced by the ordinary people in recent decades. The headcount poverty index declined from a peak level of 28.8 percent in 1995/96 to 4.1 percent 2016, according to the Department of Census and Statistics. These poverty indicators are based on the conventional poverty line which is measured only in terms of household expenditure, and therefore, do not capture the dimensions of overall quality of life, noted earlier.

It should be noted that a considerable proportion of non-poor population is concentrated just above the poverty line, and therefore, a marginal decline in their income can cause many of them to fall into the poor group, resulting in a substantial increase in the poverty incidence. The wide disparity of poverty across districts is also a matter of concern. Income inequality remains another major socioeconomic problem. The per capita income of the poorest 10 percent of the population is only around $ 200, which is just about 5 percent of the country’s per capita income of $ 3,800. The average daily income of the poorest 10 percent is around $ 0.53 vis-à-vis $ 12.00, received by the richest 10 percent. The share of household income of the poorest 10 percent is only 4.9 percent as against the richest 20 percent whose income share is as much as 53.2 percent. The rate of unemployment is down to 4.1 percent, according to the Department of Census and Statistics. Nevertheless, it is disturbing to note the high rates of unemployment among the youth and the educated. The unemployment problem would have been worse if not for the expansion of public sector employment and worker migration in recent decades. Both are unsustainable in the long run. This reflects the fact that the economy has not expanded fast enough to absorb the growing labour force.

Severe economic setback

The real GDP growth in 2017 was only 3.1 percent, and this is much lower than the growth rate of 5.0 percent projected in the government’s medium-term macroeconomic framework. It also contrasts with the great expectations of the Vision 2025, which envisaged an annual GDP growth rate of 8 percent over the three-year period 2018-2020. Sectoral disaggregation of GDP growth reflects the fragility of the economy. The main drivers of economic growth have been services and construction. The service activities which have the major share of 56 percent of GDP grew by 3.2 percent in 2017. The main service activities include trading, transport, financial services, real estate development and public administration. Heavy dependence on such activities is not a healthy sign. The industrial production which has a GDP share of 30 percent is reported to have increased by 3.9 percent in 2017. However, the industrial sector includes construction and utility services, according to the classification of the Department of Census and Statistics. When such items are excluded, the industrial sector contributes only 17 percent to the GDP. Even these limited industrial activities mainly consist of food and beverages, garments and furniture manufacturing. Such basic manufacturing is insufficient to uplift the economy.

It is only through high-tech industries based on the knowledge economic structure that a country can sustain export competitiveness so as to graduate the economy to higher stages. Sri Lanka has failed badly in this respect due to multifold factors including political instability, inconsistent economic policies, poor research and development facilities, corruption and lack of economic vision.

[caption id="attachment_921" align="alignleft" width="3500"]

It should be noted that a considerable proportion of non-poor population is concentrated just above the poverty line, and therefore, a marginal decline in their income can cause many of them to fall into the poor group, resulting in a substantial increase in the poverty incidence. The wide disparity of poverty across districts is also a matter of concern. Income inequality remains another major socioeconomic problem. The per capita income of the poorest 10 percent of the population is only around $ 200, which is just about 5 percent of the country’s per capita income of $ 3,800. The average daily income of the poorest 10 percent is around $ 0.53 vis-à-vis $ 12.00, received by the richest 10 percent. The share of household income of the poorest 10 percent is only 4.9 percent as against the richest 20 percent whose income share is as much as 53.2 percent. The rate of unemployment is down to 4.1 percent, according to the Department of Census and Statistics. Nevertheless, it is disturbing to note the high rates of unemployment among the youth and the educated. The unemployment problem would have been worse if not for the expansion of public sector employment and worker migration in recent decades. Both are unsustainable in the long run. This reflects the fact that the economy has not expanded fast enough to absorb the growing labour force.

Severe economic setback

The real GDP growth in 2017 was only 3.1 percent, and this is much lower than the growth rate of 5.0 percent projected in the government’s medium-term macroeconomic framework. It also contrasts with the great expectations of the Vision 2025, which envisaged an annual GDP growth rate of 8 percent over the three-year period 2018-2020. Sectoral disaggregation of GDP growth reflects the fragility of the economy. The main drivers of economic growth have been services and construction. The service activities which have the major share of 56 percent of GDP grew by 3.2 percent in 2017. The main service activities include trading, transport, financial services, real estate development and public administration. Heavy dependence on such activities is not a healthy sign. The industrial production which has a GDP share of 30 percent is reported to have increased by 3.9 percent in 2017. However, the industrial sector includes construction and utility services, according to the classification of the Department of Census and Statistics. When such items are excluded, the industrial sector contributes only 17 percent to the GDP. Even these limited industrial activities mainly consist of food and beverages, garments and furniture manufacturing. Such basic manufacturing is insufficient to uplift the economy.

It is only through high-tech industries based on the knowledge economic structure that a country can sustain export competitiveness so as to graduate the economy to higher stages. Sri Lanka has failed badly in this respect due to multifold factors including political instability, inconsistent economic policies, poor research and development facilities, corruption and lack of economic vision.

[caption id="attachment_921" align="alignleft" width="3500"] The average daily income of the poorest 10% is around $ 0.53[/caption]

Knowledge economy not forthcoming

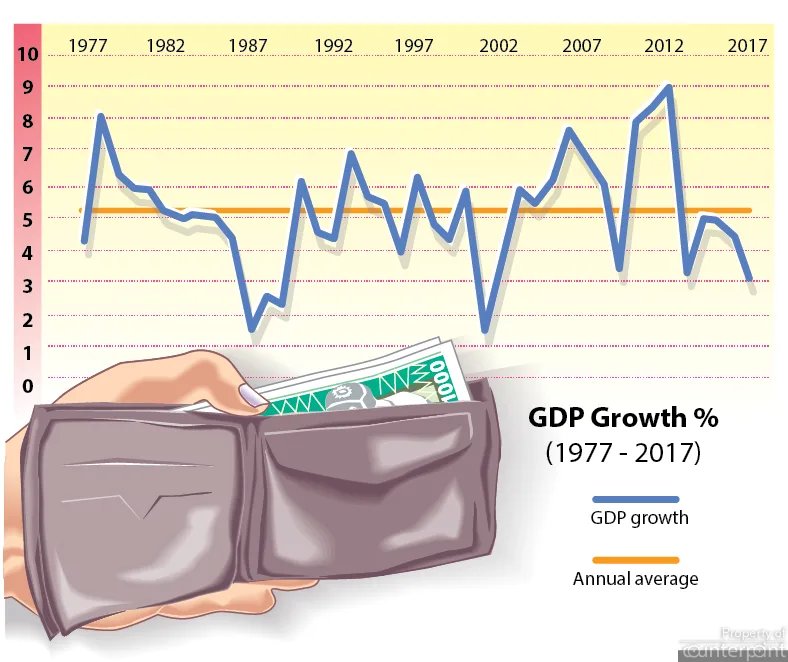

Sri Lanka’s average growth has remained around 5 percent throughout the post-liberalization period as shown in the Chart. This is the maximum growth potential of the economy. It is insufficient to tackle the problems of unemployment, poverty and income inequality, discussed earlier. The country needs to achieve a growth rate of 8–10 percent so as to absorb the young labour force, and to uplift the per capita income. For this purpose, the production structure should graduate from the traditional ‘factor-driven’ growth characterized by basic industries to modern ‘technology and innovation-driven’ growth led by high-tech industries. This calls for a knowledge-based economy. A successful knowledge economy is characterized by close links with science and technology, and high priority placed on innovation for economic growth as well as for export competitiveness.

Research and development (R&D) is a key driver of knowledge economy. Sri Lanka has made very little progress in transiting towards a knowledge economy, whereas the fast-growing Asian countries such as Japan, South Korea, China, Singapore, Malaysia and Thailand have performed much better. Sri Lanka’s position in the country ranking in terms of the Knowledge Economy Index compiled by the World Bank is not very satisfactory. Sri Lanka has to take huge strides to evolve a modern knowledge-based economy. The status of the economy in terms of other yardsticks such as the doing business index and credit ratings is not very promising either.

[caption id="attachment_923" align="alignleft" width="2000"]

The average daily income of the poorest 10% is around $ 0.53[/caption]

Knowledge economy not forthcoming

Sri Lanka’s average growth has remained around 5 percent throughout the post-liberalization period as shown in the Chart. This is the maximum growth potential of the economy. It is insufficient to tackle the problems of unemployment, poverty and income inequality, discussed earlier. The country needs to achieve a growth rate of 8–10 percent so as to absorb the young labour force, and to uplift the per capita income. For this purpose, the production structure should graduate from the traditional ‘factor-driven’ growth characterized by basic industries to modern ‘technology and innovation-driven’ growth led by high-tech industries. This calls for a knowledge-based economy. A successful knowledge economy is characterized by close links with science and technology, and high priority placed on innovation for economic growth as well as for export competitiveness.

Research and development (R&D) is a key driver of knowledge economy. Sri Lanka has made very little progress in transiting towards a knowledge economy, whereas the fast-growing Asian countries such as Japan, South Korea, China, Singapore, Malaysia and Thailand have performed much better. Sri Lanka’s position in the country ranking in terms of the Knowledge Economy Index compiled by the World Bank is not very satisfactory. Sri Lanka has to take huge strides to evolve a modern knowledge-based economy. The status of the economy in terms of other yardsticks such as the doing business index and credit ratings is not very promising either.

[caption id="attachment_923" align="alignleft" width="2000"] Former Finance Minister Ravi Karunanayake with President Sirisena.[/caption]

Future outlook is bleak

Sri Lanka is caught in a grave debt trap. The country’s public debt to GDP ratio remains around 85 percent, and it is much higher than the average for emerging economies (57 percent excluding oil producing countries). The total external debt is around 60 percent of the GDP. Public sector external debt is about 36 percent of the GDP, while the private sector external debt which has increased steadily in recent years now stands at around 24 percent of the GDP. The largest ever debt servicing commitments clustered from this year onwards is a formidable challenge. The continuing foreign borrowing by the government, including the most recent US dollar 2.5 billion sovereign bond offer, will lead to the accumulation of the debt service obligation heavily over the next decade. Given the economic setback, dismal export performance and fiscal vulnerabilities the country’s debt sustainability faces major risks.

The prolonged political instability has compounded the economic crisis. The government has failed to implement the inevitable economic reforms due to conflicting views among the coalition political parties. Political uncertainties have immense repercussions on the investment climate, particularly on foreign investment.

Former Finance Minister Ravi Karunanayake with President Sirisena.[/caption]

Future outlook is bleak

Sri Lanka is caught in a grave debt trap. The country’s public debt to GDP ratio remains around 85 percent, and it is much higher than the average for emerging economies (57 percent excluding oil producing countries). The total external debt is around 60 percent of the GDP. Public sector external debt is about 36 percent of the GDP, while the private sector external debt which has increased steadily in recent years now stands at around 24 percent of the GDP. The largest ever debt servicing commitments clustered from this year onwards is a formidable challenge. The continuing foreign borrowing by the government, including the most recent US dollar 2.5 billion sovereign bond offer, will lead to the accumulation of the debt service obligation heavily over the next decade. Given the economic setback, dismal export performance and fiscal vulnerabilities the country’s debt sustainability faces major risks.

The prolonged political instability has compounded the economic crisis. The government has failed to implement the inevitable economic reforms due to conflicting views among the coalition political parties. Political uncertainties have immense repercussions on the investment climate, particularly on foreign investment.

Unemployment is highest amongst the youth and the educated.[/caption]

Political interests take precedence over economic compulsions

In Sri Lanka, little attention is paid to economic realities in the midst of the continuing political turmoil. As a result, the country has failed to reap the benefits of economic liberalisation over the last four decades, while many neighboring countries are forging ahead with faster economic growth though they launched economic liberalization much later. The bitter truth is that there are no short cuts to economic growth or development. It is only through the hard way that we can achieve it. The longer we postpone taking corrective steps the longer we have to wait for economic progress. The political economy has considerable bearing on socioeconomic development, as it is the political authority that ultimately determines development policies. These policies are not always optimal, and very often, politicians take the decisions at discretion for their own political survival, with a short-term focus ignoring long-term economic repercussions.

To satisfy voters in a bid to retain power, politicians have a tendency to offer various welfare benefits to households at every election, such as handouts, cash transfers and food subsidies and to also create jobs in the public sector. Such populist policy preferences invariably lead to an increase in government expenditure, budget deficit, public debt, the money supply, inflation and balance of payments deficits. The outcomes are the high cost of living, food shortages, subsidy cuts and various other hardships. Although the masses, particularly the poor, are said to be the beneficiaries of populist policies, they are the most adversely affected group due to the second-round effects of such policies. The much-needed structural reforms relating to foreign trade, foreign investment, state-owned enterprises and fiscal consolidation have been neglected over the decades. The results have been catastrophic. Economic growth never picked up to ease the problems of unemployment, poverty and income inequality. Also, the economy has been subject to severe instability due to budget and balance of payment deficits.

Mismanaging the economy

The current government has failed to adopt necessary economic policy strategies and structural reforms to address the above-mentioned growth setback and macroeconomic instability. The PM has presented several economic policy statements to Parliament from time to time, but to no avail. They contained some optimistic economic targets without any action plans. Most of the proposals mentioned in those statements were not implemented. They are also at variance with the proposals, contained in the consecutive budget speeches. Similar weaknesses could be found in the policy document titled, ‘Vision-2025: A Country Enriched’, launched by the government in August last year. The launching event seemed to have been designed to attract the youth with choreographic acts in an ultra-modern stage setting. Several youth who appeared on the stage, along with the President and the Prime Minister, posed some questions to the two leaders. The V2025 booklet, consisting of around 50 pages, had a long wish list to be fulfilled during the next 8 years. Surprisingly, it does not elaborate on the specific policy strategies to be implemented to achieve the envisaged objectives. It also does not contain any statistical tables or charts which would have been useful to substantiate the facts behind the Vision. The document looked more like a hurriedly-prepared election manifesto than a coherent policy document addressing the structural weaknesses in the economy. It contains a long list of “We will …” statements. This implicitly indicates that the political authorities are yet to introduce the much-needed policies. The Vision 2025 document states, “Over the next three years, within the 2025 Vision, we will implement a comprehensive economic strategy to address constraints to growth. We will aim to raise per capita income to USD 5,000 per year, create one million jobs, increase FDI to USD 5 billion per year and double exports to USD 20 billion per year. These intermediate targets lay the foundation for our Vision 2025: Sri Lanka to become an upper-middle income country.”

[caption id="attachment_920" align="alignleft" width="2500"] The newly put together National Economic Council, appointed and Chaired by President Sirisena will supersede the Cabinet Committee on Economic Management, chaired by Prime Minister Wickremesinghe.[/caption]

These are unattainable optimistic targets, as has been argued previously in my newspaper articles. However, the fate of this Vision document is unknown today. The outcome of the high-profile Sri Lanka Economic Forum held in Colombo in January 2016, too, is not evident. Several presentations were made at the Forum by some prominent experts from Harvard. As I reiterated in my newspaper columns, those presentations were mere reproductions of the age-old textbook stuff relating to export-constrained economic growth, low government revenue, structural transformation, urbanization and economic growth. However, all those grand events seem to have been forgotten by the policymakers now. Such foreign experts hardly offered any policy options to help overcome the economic problems facing a developing country like Sri Lanka. The ill-advised policies based on such deliberations are bound to have disastrous spill-over effects in the future for which no one would be held accountable, and the ordinary citizens will have to pay the price. This is the tragedy of the voiceless common people.

Recently, President Sirisena appointed a new National Economic Council (NEC) under his chairmanship to take key decisions on all the economic and development projects of the government.

The NEC is said to supersede the Cabinet Committee on Economic Management (CCEM), which is chaired by PM Wickremesinghe. It is not yet clear how these parallel bodies would demarcate their functions and duties. All these point to market uncertainties deterring the country’s potential to ease the hardships faced by the ordinary people, as discussed below.

Socioeconomic problems aggravating

Poverty, income disparities and unemployment are some of the burning socioeconomic problems, faced by the ordinary people in recent decades. The headcount poverty index declined from a peak level of 28.8 percent in 1995/96 to 4.1 percent 2016, according to the Department of Census and Statistics. These poverty indicators are based on the conventional poverty line which is measured only in terms of household expenditure, and therefore, do not capture the dimensions of overall quality of life, noted earlier.

It should be noted that a considerable proportion of non-poor population is concentrated just above the poverty line, and therefore, a marginal decline in their income can cause many of them to fall into the poor group, resulting in a substantial increase in the poverty incidence. The wide disparity of poverty across districts is also a matter of concern. Income inequality remains another major socioeconomic problem. The per capita income of the poorest 10 percent of the population is only around $ 200, which is just about 5 percent of the country’s per capita income of $ 3,800. The average daily income of the poorest 10 percent is around $ 0.53 vis-à-vis $ 12.00, received by the richest 10 percent. The share of household income of the poorest 10 percent is only 4.9 percent as against the richest 20 percent whose income share is as much as 53.2 percent. The rate of unemployment is down to 4.1 percent, according to the Department of Census and Statistics. Nevertheless, it is disturbing to note the high rates of unemployment among the youth and the educated. The unemployment problem would have been worse if not for the expansion of public sector employment and worker migration in recent decades. Both are unsustainable in the long run. This reflects the fact that the economy has not expanded fast enough to absorb the growing labour force.

Severe economic setback

The real GDP growth in 2017 was only 3.1 percent, and this is much lower than the growth rate of 5.0 percent projected in the government’s medium-term macroeconomic framework. It also contrasts with the great expectations of the Vision 2025, which envisaged an annual GDP growth rate of 8 percent over the three-year period 2018-2020. Sectoral disaggregation of GDP growth reflects the fragility of the economy. The main drivers of economic growth have been services and construction. The service activities which have the major share of 56 percent of GDP grew by 3.2 percent in 2017. The main service activities include trading, transport, financial services, real estate development and public administration. Heavy dependence on such activities is not a healthy sign. The industrial production which has a GDP share of 30 percent is reported to have increased by 3.9 percent in 2017. However, the industrial sector includes construction and utility services, according to the classification of the Department of Census and Statistics. When such items are excluded, the industrial sector contributes only 17 percent to the GDP. Even these limited industrial activities mainly consist of food and beverages, garments and furniture manufacturing. Such basic manufacturing is insufficient to uplift the economy.

It is only through high-tech industries based on the knowledge economic structure that a country can sustain export competitiveness so as to graduate the economy to higher stages. Sri Lanka has failed badly in this respect due to multifold factors including political instability, inconsistent economic policies, poor research and development facilities, corruption and lack of economic vision.

[caption id="attachment_921" align="alignleft" width="3500"] The average daily income of the poorest 10% is around $ 0.53[/caption]

Knowledge economy not forthcoming

Sri Lanka’s average growth has remained around 5 percent throughout the post-liberalization period as shown in the Chart. This is the maximum growth potential of the economy. It is insufficient to tackle the problems of unemployment, poverty and income inequality, discussed earlier. The country needs to achieve a growth rate of 8–10 percent so as to absorb the young labour force, and to uplift the per capita income. For this purpose, the production structure should graduate from the traditional ‘factor-driven’ growth characterized by basic industries to modern ‘technology and innovation-driven’ growth led by high-tech industries. This calls for a knowledge-based economy. A successful knowledge economy is characterized by close links with science and technology, and high priority placed on innovation for economic growth as well as for export competitiveness.

Research and development (R&D) is a key driver of knowledge economy. Sri Lanka has made very little progress in transiting towards a knowledge economy, whereas the fast-growing Asian countries such as Japan, South Korea, China, Singapore, Malaysia and Thailand have performed much better. Sri Lanka’s position in the country ranking in terms of the Knowledge Economy Index compiled by the World Bank is not very satisfactory. Sri Lanka has to take huge strides to evolve a modern knowledge-based economy. The status of the economy in terms of other yardsticks such as the doing business index and credit ratings is not very promising either.

[caption id="attachment_923" align="alignleft" width="2000"] Former Finance Minister Ravi Karunanayake with President Sirisena.[/caption]

Future outlook is bleak

Sri Lanka is caught in a grave debt trap. The country’s public debt to GDP ratio remains around 85 percent, and it is much higher than the average for emerging economies (57 percent excluding oil producing countries). The total external debt is around 60 percent of the GDP. Public sector external debt is about 36 percent of the GDP, while the private sector external debt which has increased steadily in recent years now stands at around 24 percent of the GDP. The largest ever debt servicing commitments clustered from this year onwards is a formidable challenge. The continuing foreign borrowing by the government, including the most recent US dollar 2.5 billion sovereign bond offer, will lead to the accumulation of the debt service obligation heavily over the next decade. Given the economic setback, dismal export performance and fiscal vulnerabilities the country’s debt sustainability faces major risks.

The prolonged political instability has compounded the economic crisis. The government has failed to implement the inevitable economic reforms due to conflicting views among the coalition political parties. Political uncertainties have immense repercussions on the investment climate, particularly on foreign investment.RELATED NEWS

View all